Contemplating the end of 2023 and the start of 2024, let’s take a look at the differences between creating and keeping wealth. It is actually not that hard ridiculously easy to deplete the wealth you have sweated for, in most cases, decades to create. The Vanderbilts (read about this here and here) are a well-known example.

Is sustaining more difficult than creating? Yes. There are many uncontrollable variables during this period of your life when you are most typically consuming cashflow from investments rather than creating cashflow and investments by working.

Inflation, unplanned expenses, sequences of investment returns, and living longer than planned all cause cash consumption to be challenging to predict. The cashflow you create by your own labor and/or intellectual property can largely offset (assuming you save!) the fluctuations in these variables - while you are working. You can always choose to earn an income for another year or two or three (most of the time). You can gradually reduce (this is behaviorally hard to do, BTW) your spending over time as you prepare to live off your accumulated investments. In contrast, most folk who have stopped working loathe to return to work, and rapid changes in spending tend to be quite difficult to apply and then sustain.

Then there are the emotional factors. How much did you sacrifice to get here? How do you feel about not doing something now when you have waited so long to have the time to do this thing? How likely are you to respond positively to a need to reduce spending now in order to decrease the probability that you will run out of money in the future?

Creating

Comparatively, this is the “easy” part. Figure out how much you can save. Determine how much you should be saving. Decide how much you will save. Automate your saving. Set an investment strategy (my subversive belief here is that most any strategy will work so long as you stick with it) that is consistent with your tolerance for volatility and amount of time before you plan to start withdrawing from or living on the income from your investments.

The math of this is pretty straightforward, if you believe that long-term market rates of return are likely to repeat themselves, on average, over long periods (which I define as 20+ years). All the data we have gathered since 1858 points this way, and while the future may be different, it seems unlikely at this point.

Here is a calculator you can use to calculate the result of a savings scenario. All of the following data was calculated using the investor.gov compound interest calculator.

By the way, if the monthly amount in this case is $2,500, which is a pretty common amount for someone who is making maximum 401(k) contributions and has some form of employer match, the 20 year result is about $2 million (and it is $4.8 million if you have 30 years).

The hard part of this easy part is your discipline. Each year there is invariably an unplanned expense of some kind. I like to call this the nearly certain, annually reoccurring, “unexpected” expense. This can derail your thinking into something like: “I can never plan accurately, so keeping a spending plan is a waste of time”. Once your thinking is derailed, your actions are soon to follow. My advice is to have an unplanned line item in your spending plan. This is a form of contingency planning. The only thing we can really plan for is that our plans will be inaccurate, so we might as well allow for this and expect it. The good news? First, by assuming your plan will be derailed, your thinking has a good chance of staying on the the tracks. Second, if you do not use this money, your savings plan is enhanced for the year - if you have the discipline.

The big factor is compounding - just look at the curve. Your saving is constant, and in these cases we, conservatively, did not increase your saved amount over time. The lesson? Never Interrupt Compounding. This takes discipline - saving every month and every year, leaving your money alone, and letting work. And yes, this means during down markets, too.

The best way to maintain discipline is to automate your saving. Your institutional retirement plan (401(k), 403(b), etc.) works so well precisely because, each pay period, a fixed percentage or dollar amount is removed from your compensation, before you ever see it, and placed in the plan. In addition, in most cases, prior to age 59 1/2, there is a significant tax cost if you withdraw money from the plan. These behavioral nudges (more here) drive discipline.

Assuming you need to save in addition to your retirement plan, you are best served by automating that saving, too. Automate a scheduled transfer from your checking account, each time you get paid, into your investment account. Have an automatic process to invest those dollars as they are periodically deposited.

There is a tremendous, added benefit to doing this. If you are saving “enough” (and there is lots to talk about regarding this word) and on the path to funded contentment1, you can spend the remainder with confidence and abandon. Want to own a Veyron or a 365GTB/4 Daytona? Go ahead - if you have already saved what you need to save (and yes, I think the Veyron is physically ugly, but you can spend lots of money on one, and it is so dang fast I almost don’t care what it looks like).

Sustaining

You have done it. Reached the goal line. There is enough wealth that you can live off some combination of pension (unlikely for most of us, I know), Social Security (which many do not believe they will receive, but for those in their late 50’s and beyond it is at least, for now, highly probable) and investment earnings and liquidations.

Life is easy. Well, if you are the one accountable for making sure that the family never runs out of money, no matter what happens and regardless of how long this period is, it not only feels challenging, it is.

The goal line is actually the great wide open of financial planning. The end game cannot be known. Dealing with your particular sample size of N = 1, we cannot forecast how long you will live. At best, we can determine a range, and there will still be 1% or so of people that fall outside of a quite wide range. The oldest person we know of, so far, made it to 122 (data here)! So when a client tells me there is no way they will make it past 85, I listen and then plot a plan to at least age 100, knowing that this may not be long enough - and if it is too long, well someone is getting something, which is not an awful outcome. I suspect that within the next ten years we will be advocating running financial plans to age 110.

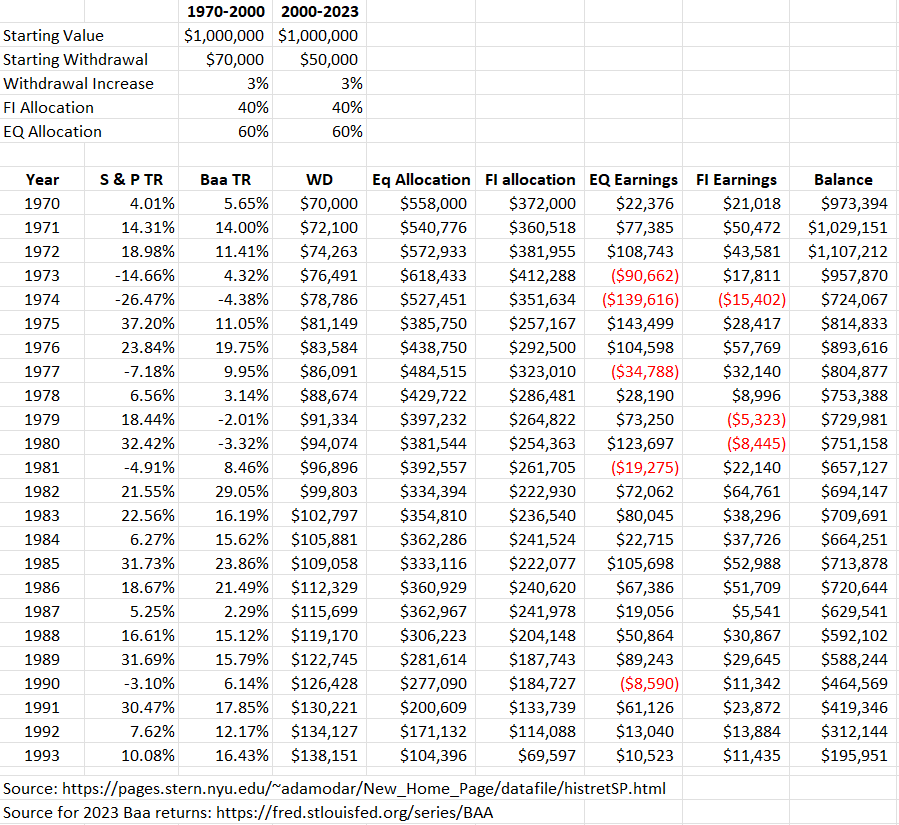

We cannot know the future and/or sequence of investment returns. The sequence, especially in the first few years of consuming your wealth, has a tremendous impact, positive or negative, on your long-term outcome (see article here). Below are some tables I built using total returns of the S & P 500 and the Baa corporate bond index. In both cases, we assumed the cost of living increases 3% annually and that the withdrawal was a fixed percentage of the initial portfolio, adjusted for inflation. We are, for simplicity, ignoring tax effects.

1970 through 1972 rewarded, enormously, someone who began living off their market investments. If you had withdrawn 5% of the initial portfolio balance, inflation adjusted, by 1993 you would have had 3.9 times more money than when you started. If you had known the future, you could have withdrawn 7% (!!!) of your initial portfolio balance, inflation adjusted, and still had $195,000 of your initial $1 million balance after 24 years. This is an outstanding result, although if you lived to year 26 you would have run out of money.

2000 through 2002 did the opposite. Your withdrawal would have been limited to 5% (which, historically, is not bad!), and at the end of 24 years your $1 million portfolio would have been $$192,000. Also of note, with a lower withdrawal rate you would still have run out in 27 years.

Here’s what would have happened if you tried a 7% withdrawal rate from 2000-2023: You go broke in 2014. 5% was risky. 7%? Financial suicide.

I intentionally selected periods that would create a contrast of results. The point is that we cannot know what you will experience. We cannot know how long you will live. Is 24 years long enough? Maybe. Maybe not. When do you start drawing income? If it is age 55, I would want to plan for at least 35 years, and that is the absolute minimum. I would not like the “could go broke” risk profile of a 24-year income plan, although you may be comfortable with it. Even at age 65 I want to see at least 30 years. Who wants to be 92, healthy, and 3 years from going broke?

Yes, you probably own a home, and that is an asset that could be sold to fund income and some form of rental or assisted living home. Speaking of that, might you need assistance as you age? Probably. How will that be paid for? Will you reduce spending enough to cover it? Might you need to set aside dollars, or perhaps buy insurance, to pay for this? The data says this is a good idea. Do we know what your situation is going to be? Again, we can neither predict what will happen in your lifetime nor do we know the associated cost of future events. Scenario planning is crucial.

Simply maintaining income, even if the goal is to bounce your first check on your last day alive, is difficult. If we are talking about substantial, what you might think of as “unspendable”, excess wealth, well, that comes with both the “staying alive” issues and many other potential issues (take a look at this Wall Street Journal article about the Angelos family). Now you bring in all the family considerations, often spanning multiple generations, where you are also dealing with things like equitable distribution (and let’s understand that “equitable” is behaviorally in the eye of the receivers). There may be local, state, and federal estate tax payments to make, which, if you have illiquid assets like a baseball team, can destroy the estate (hello, Prince - read about the estate here, Michael Jackson, and Jack Kent Cooke, to name but a few of these cases). I will not cover excess wealth issues in more depth. There are entire books written about this process.

Can it feel like being out in the ocean, with no land in sight and unpredictable wave patterns? Sure.

Shelter From the Storm

Clearly I am a champion of planning. I am a greater champion of re-planning. Realistically, your plan is “wrong” not but a few months, at most, from when it is crafted. Given all the variables, it was, arguably, never “right”. Too many things change. A consistent, repetitive, collaborative (with a team of estate and business attorneys, CPA, financial, and other advisors, as appropriate) process is 100% the best approach we have at this time. The timing of that process depends on the complexity of your life. The more successful you are, the more complex your life, the more often your plan needs a review. What works best for you is unique to your situation, behaviors, and the dynamics of your family and/or business partners.

Thanks for reading.

Sundry

The most moving song I listened to this week

I finished “I Have Some Questions for You”. Teen angst, murder, boarding school, various careers, and adult relationships all rolled up into one story. Wow.

We have an awful lot of of extremely positive economic news this days, and that’s a good thing. You can listen to one view here. Here is another. There are doomer views, too, although those narratives and data interpretations are not supported by the actual results.

You might have picked up that I do not think there is a universal/safe/sustainable withdrawal rate that can be applied for income planning. Each person’s situation is unique, and what works for that person or family cannot be condensed down to a 4%, or 3.62%, or 5% (or, pick your number) withdrawal rate. There’s nothing wrong with the research. It’s just that the research can only look backward at what happened and there is nothing predictable about our lives or the investment markets, or inflation, or taxes, or Social Security.

The Geometry of Wealth, Brian Portnoy

Much thanks for your blog and the videos!