The Uncertainty of Business Partnerships

The Uncertainty of Business Partnerships

Dan Snyder Shows That Breaking Up Can Be Hard to Do

I bet the NFL wishes it never admitted Dan Snyder to the league. In developments this week, it appears that there is a significant dispute between Mr. Snyder and the NFL regarding indemnification (there are others, but I don’t want to repeat Sally Jenkins - you can read her here, with more here). It makes me wonder whether the NFL owners’ agreement contains a hold harmless clause . While I am not an attorney, I did stay in a Holiday Inn Express last night. It is awfully common for agreements to have a bi-lateral clause. That is, you are not responsible for bad acts on my part, and in return, I am not responsible for bad acts on your part. Maybe there is a clause and the NFL, now seeing (or at least admitting to itself) a series of bad acts, wants out of the clause and wants Mr. Snyder to compensate the NFL for the NFL’s possible liabilities. Maybe Mr. Snyder wants the NFL owners to share his pain should he be liable for damages or restitution for financial fraud during his ownership tenure. Or maybe there is no clause at all. I do not know the facts, other than there appears to be a dispute. Any of these are possible.

In any case, having already spent a lot of time in court, it looks like Mr. Snyder and the NFL are both going to be spending more time there. Even if that does not happen, all of the press reflects badly on both parties, regardless of who is the instigator or at fault.

Here’s the thing: breaking up a partnership (the NFL is, technically, a trade association financed by its teams, with lots of shared revenue and expenses, although to me it sure seems to have the behaviors and issues of a partnership) is hard to do. Businesses are made up of people. People are not predictable. People are full of biases and irrationality, can change substantially over time, and have a tendency and the desire to craft a narrative matching our view of ourselves, what we want to believe, and our desired outcome.

How It Started

You worked with someone, or you got to know them well through your kids, or something. There is a shared business philosophy and a passion for the same product or service. They are an innovative thinker and perhaps a brilliant operator or financially savvy. Something is there that you see as a unique skill or capability. They see the same in you. One of you has capital and the other product or skill. Maybe it is all of the above. It’s perfect. You form a business.

The business flourishes. Man, life is good. Until it isn’t. Strong fences make good neighbors. There is an awful lot of value and truth in this timeworn statement.

How It’s Going

Running a successful small business is hard. It can be and usually is somewhat chaotic every day. When the business is not going well, it is incredibly difficult.

Your partner (or you, for that matter) becomes an alcoholic/addict. There is an intra-office affair and a related, nasty divorce with your partner debasing the brand as a result or is simply not present for months. Embezzlement. One of you dies unexpectedly or is sick or injured and unable to work. There is a disagreement about who is making the larger contribution and a subsequent argument about net income allocation. There is undistributed net income, no distribution to allow for individual partner tax consequences, and one of your partners needs cash to pay their tax bill. There is a need for capital and one of you is not able to make the contribution. Business conditions become seriously negative and require additional commitment or expertise. You think I am being negative? Not a chance. I am citing things I have seen in my 36 years as a business consultant and financial advisor.

Here is one I had to work through with a client. The operating agreement poorly addressed transfer of shares at death and one partner died unexpectedly. At death, the shares became part of the deceased’s estate. The partner’s estate plan distributed 50% of the shares to the spouse and 50% to the deceased’s sister, neither of whom understood the business. The surviving partner continued to run the business and chose to not distribute net income. The inheritors got the (pass-through) tax bill and no income. The operating agreement defined neither a specific, funded buy-out at death nor did it require distributions to pay personal taxes due. The two inheritors went through a multi-year court battle to obtain their shares of net income and also to be able to sell their shares (at a much-discounted value). In the interim, they had to pay taxes on undistributed income as well as legal fees. This is on top of the emotional trauma of the unexpected death of their spouse and sibling, respectively.

How It Ends

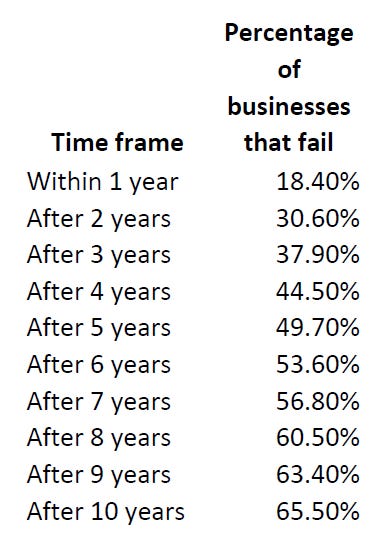

Often, as above, it ends poorly. A legal proceeding, financial issues, and loss of years of hard work and expected value may result. Sometimes, bankruptcy. As you can see here, it is common to fail.

Source: Lending Tree: The Percentage of Businesses That Fail and How to Boost Your Chances of Success

You are going to decide how it ends at formation, during the life of the business, or in some sort of process, maybe negotiated, maybe court, at the point of failure. My position is that the right time is at formation. It can be awfully hard to make operating agreement changes while you are running the business. However, it is also common to make agreement changes during the life of the business as the business grows and evolves, and well-structured businesses/strong partnerships can do this. This, though, is doggone hard to do if you did not begin with a sound agreement and a philosophy that the agreement is important.

You must anticipate and plan for the end of the business. That is not to say you should plan to fail - there is a 34.5% chance that you will be succeeding at the 10 year period. Assuming it will all go well (after all, you were lifelong friends) is not what I recommend, though. Plan for it to go well. Allow for the contingency of failure. You should be thinking of how you unwind in the most challenging of situations. Your agreement should specify exactly what happens, including any funding that may be necessary, in each scenario. For example, at death, either the entity or the partner(s) should be required to buy back the deceased partner’s shares, at a defined price, in a specified period. If the business does not have the cashflow to reasonably make that happen, perhaps you require the purchase of life insurance to fund the potential liability.

You have to assume that the end is uncertain, that you and your partner’s futures are uncertain, and that anything can happen. We can hope for the best - but cannot expect the best. We have to anticipate the worst.

Random Stuff

Thank you, all who are reading this. There are 127 people subscribing in this first month of playing in traffic.

Thank you to Penny Phillips, Bob Seawright, and Joy Lere, all of whom encouraged me to start writing.

I am currently reading Quit, by Annie Duke (Amazon link). If you think quitting is the route to failure, give this a read, or watch below.

I am reading two other books concurrently: Lyndon Johnson and the American Dream, and Come to This Court and Cry: How the Holocaust Ends. There is always much to be learned or reminded of from our past. Watching the

newsadvertising branded as news is, to me, useless. Reading history? Priceless.

Life as it is. It is good that today all problems can be solved by agreeing on them. There are many solutions and many sources. People who have problems in business need to be able to find solutions, they should definitely try https://www.nataliazubrytska.com/executive-coaching