The Grand Illusion

"I'll be back"

Cat-Scratch Fever

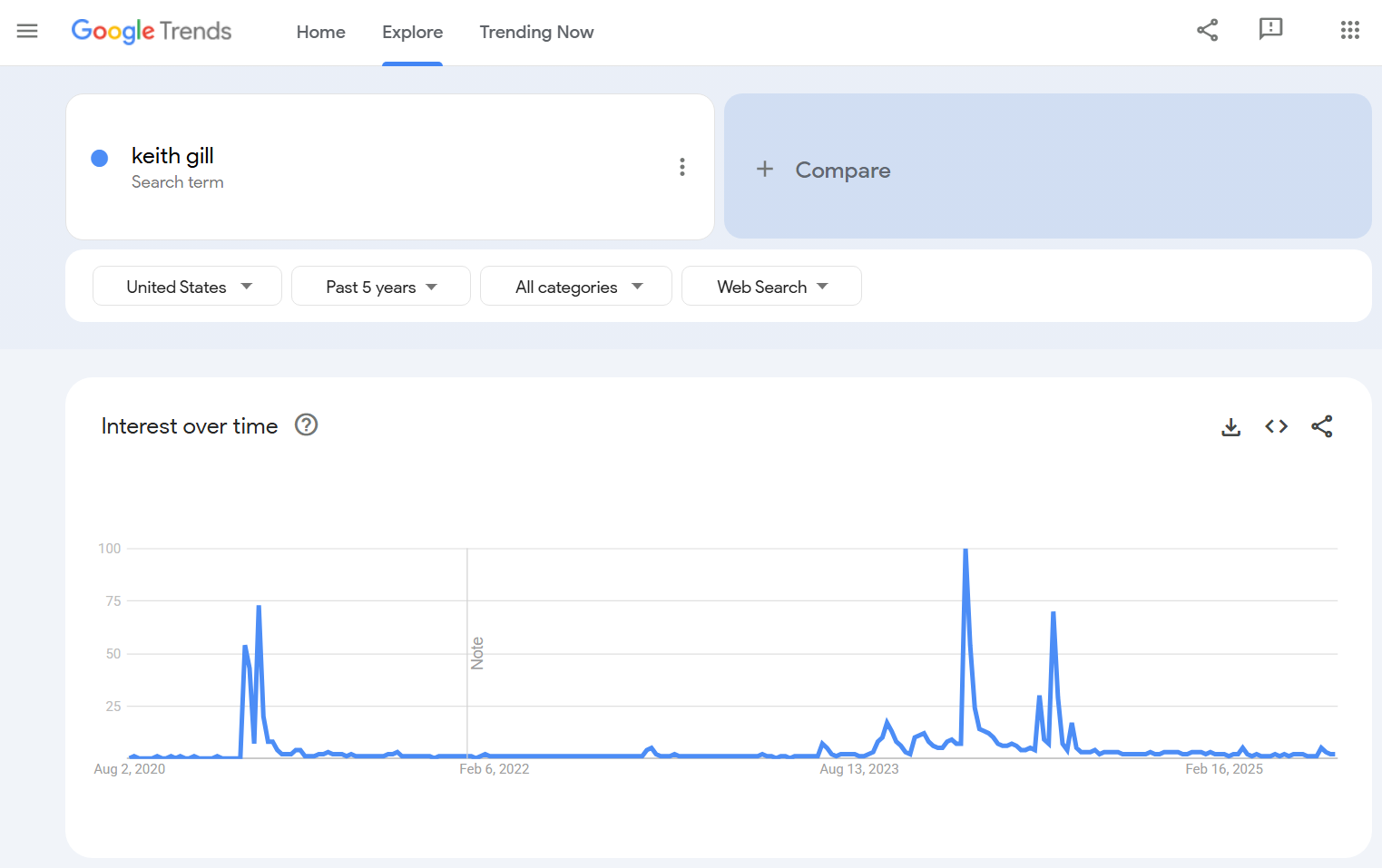

It hasn’t been exactly a long time since Roaring Kitty (Keith Gill is his real name) was, at least in the investing world, famous. Here’s a Google Trends snapshot of Keith Gill mentions, and this is not all of the media mentions, for sure.

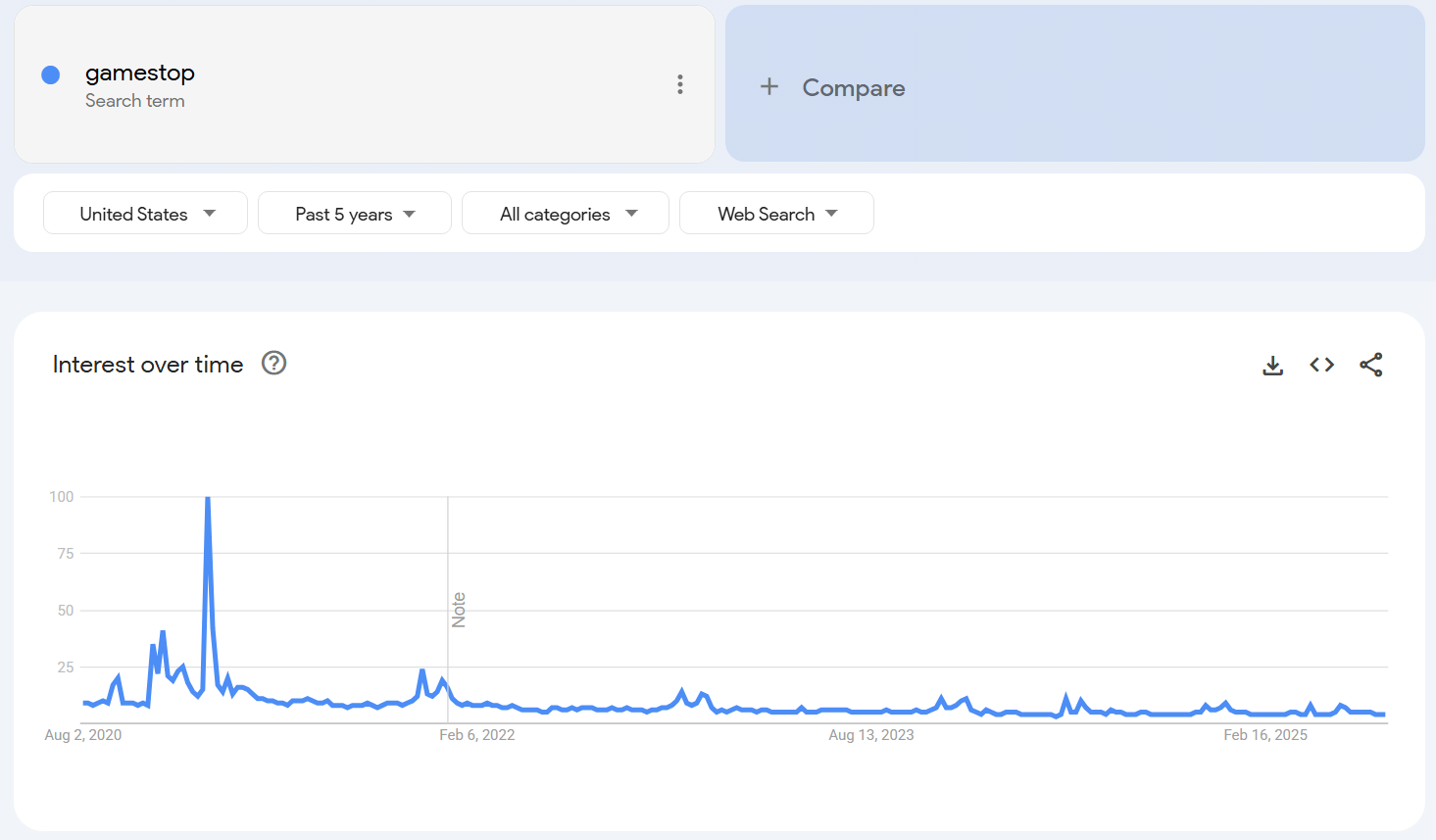

And GameStop (GME) mentions:

Here’s the stock price over the same period:

If you study the above price chart, you will note that Mr. Kitty had extraordinarily good timing (and a good time, too, I bet). That, folks, is almost always luck and not skill. If I were a devious person, I might conclude he was pimping pumping his own trade. He probably had enough followers to make that work. In the preceding 19 or so years of public ownership, GME had never been higher than $15.53, mostly hovered between $3 and $6, and was not particularly profitable. What caused this run to $75? You can say social media. You can say the financial media. What you cannot do is predict these runs, neither the start nor the end.

I can see how you might want to build a momentum trading model based on media mentions/social media volume and whether it’s positive or negative. The problem with this is the lack of facts. It’s a narrative and a meme. The trend can turn the other way (regardless of whether you are short1 or long2) in a hurry.

Also of note in the GME trade: for every winner, there were losers (and this is always true, in every trade). Some of you had a share of the ole cat’s good luck with GME, no doubt. I bet the great majority of GME traders had bad luck/timing, though. If you are not one of the people who is online, watching your particular target trade virtually every second (you can trade pretty much anything 24/7 these days), you run the risk of getting caught on the massive downside that occurs nearly every time with the meme stocks. Even if you are a trade hawk, are you disciplined enough to get out at the right time? Do you even know what the right time is, other than in hindsight?

You run the risk even if you are one of these people.

Why? The prices are illusory. In almost no case do the economics of the company support the (temporary) valuation price. The price is a narrative/meme itself. There is no supporting economic value or dividends or net income to flow through to the shareholders. It’s a trade, and the great majority of you must be lucky to profit from the trade.

The OPEN Door

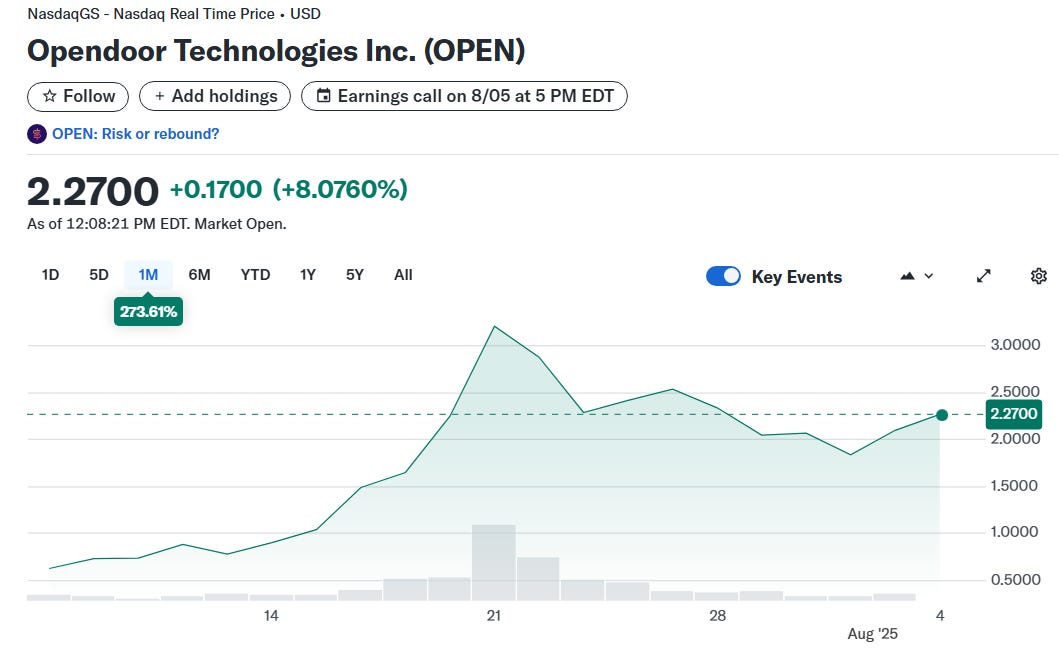

Let’s talk about OPEN for a moment. 273% gain in one month? I’ll take it. But a 273% gain is a snoozer if you got the timing right. If you bought on July 7, at the low during the day, you paid 57 cents per share. You did know this was the low, correct? You have some sixth sense or predictive model telling you this is the bottom, of course you do. You then sold at the high, on July 12, at $4.97. Your model or intuition tells you this, too, right? That’s a hypothetical $4.40 gain (ignoring taxes and trading costs) in 14 days. 7.71 times your investment. And you committed enough capital to this trade to make it meaningful, right? Because doing this with a $100 trade and ending up with $871 ain’t gonna change most of your lives - unless you can repeat it (and if you can, you ought to be trading and not reading this). By the way, the low on 7/12 was $2.61 and the close was $3.21 - either of those trades was still awfully good, but look at what you missed due to the timing!

This is precisely why I believe the meme trades are all luck. And someone does get lucky, almost every time. Just like the annual S&P predictions (my friend Bob Seawright’s Forecasting Follies, which he updates annually, is a fun and informative read), when large numbers of people are doing something, someone draws the lucky straw. The Slow Horses think they’re gonna get out of Slough House and back to Regent’s Park, and the rest of us humans remain optimistic about our trades in the most unrealistic conditions. We see that someone else benefited from luck and think it will happen for us, too. Or we believe, because we want to (hello, motivated reasoning, nice to meet you!), that it’s skill and we can do it too. And you, you know, it could happen. But the probabilities are against you. It’s much more likely that it won’t. Successful investing, for those people who don’t have a ton of excess capital, is boring (it’s often boring, or should be, for many of those who do). Not a lot of people like boring - they want their money to be (positively) exciting (money does excite the brain, and not always in a good way) and they tend to ignore the potential for negative outcomes and the anxiety or depression that may come with those outcomes. Until it happens.

If you have excess capital (defined as more than you can reasonably expect to spend in your lifetime, given your historical spending habits), you can take some investing flyers if you want. You can bear the risk, presuming your mental make up is such that you can shrug it off emotionally if you lose some or all of this excess. That doesn’t mean you should.

It’s Like You Never Left

So just what is it that’s back?

Stocks are doing crazy things again.

The share price of online house flipper Opendoor Technologies has catapulted some 377% in the past month, despite a stagnant U.S. housing market. One of the biggest stock gainers Tuesday was Kohl’s, a department store that has been losing ground to competitors for some time and has replaced its chief executive more than once in recent years.

On Wednesday, the crowd favorites were unusual names such as GoPro and Krispy Kreme, with both the camera company and doughnut maker notching eye-popping gains over the week.

The memes are definitely back, although I don’t really think they ever left. How humans think about investing does not seem to change radically over time. Note the phrase “the crowd favorites”. Just think about that.

So I try to be hip and think like the crowd

But even the crowd can't help me now3

Yale economist Irving Fisher was jubilant. “Stock prices have reached what looks like a permanently high plateau,” he rejoiced in the pages of the New York Times.

Mr. Fisher said that in 1929, folks. He was not the only learned and famous person saying so. It turns out there were a few meme stocks then, too.

The good news is that, if you were diversified (pre-crash) and had cash reserves, you most likely survived. For all of the go-to-zero stocks (there is no good data on this, although some of the records indicate that as many as 20,000 businesses failed and at least several hundred of those were publicly-held) and roughly 8,000 failed banks , you had survivors like Electric Boat, Douglass, and Honeywell. You did, however, have to hold these for 25 or so years to get these pre-tax returns. Observationally, courage and perseverance remain two of the most effective investing behaviors.

Let’s not forget the tech crash/dot-com bubble. Sock puppets, anyone?

Pets.com was an American dot-com enterprise headquartered in San Francisco, U.S, that sold pet supplies to retail customers. The website was launched in November 1998 and was shut down in November 2000. A high-profile marketing campaign gave it a widely recognized public presence, including an appearance in the 1999 Macy's Thanksgiving Day Parade and an advertisement in the 2000 Super Bowl. Its popular sock puppet advertising mascot was interviewed by People magazine and appeared on Good Morning America.

Although sales rose dramatically due to the attention, the company failed to become profitable and became known as one of the biggest victims of the dot-com crash in 2000. Since 2001, the Pets.com domain has redirected to PetSmart's website.

And then there were Webvan (it was Instacart sans vertical integration with Kroger), US Internetworking (one of my personal “learning opportunities”), and a host of others. Some survivors, like Cisco, Intel, and Oracle, dropped 80% in value during this timeframe. They were meme stocks at a point in the dot-com bubble. These three, along with many others, actually had decent economics, substantial customer bases, and great products, so they survived. Many did not. Determining the difference and making sure you focus on the most likely survivors is incredibly difficult in the exuberant times (like the SPAC craze of a few years ago). Our brains tend to follow the crowd and mislead us quite effectively during boom markets.

The Force

Like the Force, I think the Meme is with us, always. We get bored, we get flush, we get cocky - who knows the core cause, and like the ghosts in Beetlejuice we summon it with our irrational exuberance. Surprise, surprise, surprise: we get a similar result.

The Cure? Don’t play the game. Create process and habits that prevent you from playing. It’s a choice. Maybe not so shockingly, that choice is a set of boring and effective behaviors:

Spend less than you make.

Save first, spend the difference.

Select an investment strategy and stick with it.

Systematically and automatically invest - remove your brain from the repeated actions to save and invest.

Maintain an income/cash reserve.

Shameless plug: Nudges are effective. A good financial advisor will provide the appropriate nudges. These behaviors, while simple, are not easy to develop and maintain. Most of you will not naturally establish the processes or develop the habits. This is not a character flaw. These habits are not taught often and our advertising-driven media doesn’t value them much. Don’t take my word for it. Richard Thaler and Cass Sunnstein, two premier behavioral finance thinkers and researchers, wrote a book about this. Shockingly, it’s titled Nudge.

Go ahead. Reward yourself. Don’t listen to the voice. Be boring. It’s an investment you make in your future self, health, and wealth.

Selling a stock you don’t own in the hope that you can it later at a lower price. The expectation is the price will decline in the future.

Buying now with the expectation that the price of the stock will increase in the future.

Chi-lites, “Oh Girl”