Psychotic Reaction

Psychotic Reaction

Twitchy Brains "Win" in Epic Battle of Humans Versus Markets

The twitchy decisions that cost investors about 1.7% in compounded, annual returns - and some music, too.

This treatise is mostly about humans and investing. Investment strategy and execution are not financial planning. They are components of a proper financial plan. You could be a tremendously good investor and yet not achieve your desired planning outcome(s).

For a discussion on financial planning, go here (written) or here (video).

On to the show.

Investment Timing and Performance

Morningstar publishes their “Mind The Gap” analysis each year (the most recent one is here). Morningstar analyzes why investors’ performance lags the performance of the underlying investments. In every category, the investment/asset class outperformed the actual investor owning that investment/asset class.

Now, to be fair, unless you as an investor fund your investment selections on January 1 of the ten-year period, there will be a gap. Investment performance is measured on a calendar year basis: time-weighted performance. As an investor, your performance is affected by the timing of your cash flows into and out of the investment, so you experience dollar-weighted performance. This embedded difference, however, becomes relatively small over time IF you stay in your investment selections for long periods.

The more volatile the investment class, the larger the performance gap, with the smallest gap being in the “Allocation” category. Allocation funds are funds that allocate across multiple investment categories with a goal of providing a highly-diversified investment mix within a single investment selection. The “Target Date” funds that can be found in most 401(k) and other qualified retirement plans are examples of Allocation funds.

Another important aspect of dollar-weighted performance is that up and down swings, which investment professionals call volatility or risk, are not at all consistent. Missing just a few days in the markets can be extremely painful. Further complicating matters, those best days are a random walk - that is, they are statistically unpredictable as to when they may occur. Considerable quantitative effort is put into attempting to predict market patterns. At least so far, this effort has been to no avail.

The Twitchy Brain

The common theme in our investing brains is fear, frequently invoking the fight or flight mechanism, making this a powerful beast for most all investors.

Jason Zweig wrote a terrific piece: “The Seven Virtues of Great Investors” (here).

Ordinary investors are afraid of what they don’t know, as if they are navigating the world with those antique maps that labeled uncharted waters with the warning “here be dragons.” Great investors are afraid of what they do know, because they realize it might be biased, incomplete or wrong. So they never deviate from their lifelong, relentless quest to learn more.

In both cases, the investor is fearful. Whether that is fear of the unknown or fear of bias, it’s still fear and can induce poor long-term decisions.

Making a courageous investment “gives you that awful feeling you get in the pit of the stomach when you’re afraid you’re throwing good money after bad,” says investor and financial historian William Bernstein of Efficient Frontier Advisors in Eastford, Conn.

You can be pretty sure you’re manifesting courage as an investor when you listen to what your gut tells you—and then do the opposite.

Then there is the courage (overcoming fear, that is) needed to make and stick with decisions under uncertainty. Chances are quite good that, if you make a great investment decision, at least part of your success is that your timing is contrary to the majority of investors and markets. Also, whether you make a concentrated or diversified choice or set of choices, at some point the market will not reward your decision and that non-reward may stick around for a loooong time. There has been a big move towards index investing over the last 20 years or so. You can see, in this chart from Macrotrends, that the S & P 500 can be flat for many years (roughly 1999 through 2014 in this example, and lest you accuse me of cherry-picking data, take a look at 1968-1980. There are other, similar periods).

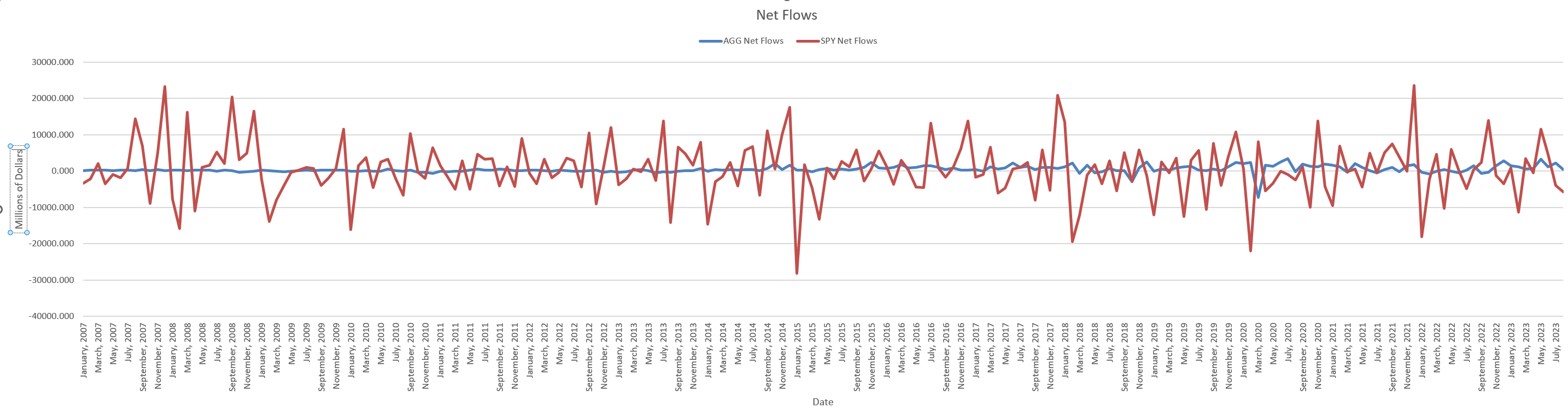

Let’s take a look at fund flows, using two widely-used funds, SPY to represent US stocks and AGG to represent US fixed income, with flow data from ETF.com. How do these match up with S and P and prime rate trends?

The S and P took a precipitous drop starting in August 2007. SPY (stocks, as represented by the S&P 500 index) fund flows in August? A positive $40 billion. So the market is heading down and folks are investing into the downturn? That would be correct. US equity markets bottomed in March 2009. How about SPY fund flows? Investors withdrew $28 billion from January through May 2009. June through August showed purchases of $2.075 billion. For the year, investors withdrew $19.88 billion from SPY. The S &P was up 68% in the period from March through December and was up 28% (!!!) for the year. Investors? Not so much.

What about bond market flows, as represented by AGG? A fundamental of bond price performance is that when interest rates go up, bond market prices go down. When interest rates go down, bond market prices go up. Why? When you own an investment that has a fixed interest rate (which is true of most bonds, with Treasury Inflation-Protected Securities - TIPS - being the major exception) and the prevailing interest rate goes up, I do not as an investor want to own the older bond, with a lower rate, when I can buy a replacement at a higher interest rate. Market prices therefore adjust: if I can buy the older bond at a discounted (reduced) price, then my yield on that bond can be made equivalent to the new bond I could buy at a higher rate. The reverse is also true.

The peak time to buy bonds in the 2007-2023 period was either 2007 or now, today. “Savvy investors” ought to have been piling into fixed income/bonds in 2007. So what did people actually do? They added about $2.75 billion. That is not exactly piling in. And as rates were falling, what did they do? In 2008 and 2009, investors purchased about $3.3 billion of fixed income. In no way did investors “rotate” from bonds to stocks or stocks to bonds in any meaningful fashion.

To summarize, a successful market-timer would have sold stocks and bought bonds in 2007, bought stocks and sold bonds in early 2009, then be buying bonds and selling stocks this year (editor’s note: we have yet to see a successful, repeatable market-timing strategy).

In other news, even if you had really poor initial timing, when you stick with it for 20 or more years, thereby removing timing from future decisions, the probability of your success becomes quite high. Put another way, lump-sum investing can be quite painful at the point in time when you do it and quite rewarding over longer periods. Systematic investing, called dollar-cost averaging by investment professionals, can feel the same way and has similar (lump-sum nearly always outperforms systematic over long periods, by the way) results.

Human Versus Market

The least volatile asset classes make the brain twitch the least. As a result, people tend to do better in comparison to the market (and we still do worse!). We trade less because we twitch less. Fixed income tends to attract steadier inflows because it is, most of the time, not subject to wide wings in valuation - except when interest rates are moving quickly. The widest gap is in sector equity funds - funds that target energy, banks/financials, or technology, for example. They tend to be the most volatile and drive the greatest twitch.

Historically, the most volatile asset classes (I am excluding crypto, for the moment, for lack of comparable data, as the history I am thinking of starts, data-wise, in 1925) provide the greatest long-term returns? You want to have great compounded returns? Focus your investment on small-capitalization and emerging markets stocks. How many people can stick with this strategy? Data says: “Not many”.

De-twitching

Looking at the data, the best way to decouple your behavior from your investments is an allocation fund or strategy - “set it and forget it”. That does have its own issues, though. From my friend Brian Portnoy: “Diversification means always having to say you’re sorry”. It takes significant courage to stick with an investment strategy when “it’s not working”, and any strategy can “not work”, often for years. An allocation/diversified strategy (talking my book here - this what we do for our clients and is how I personally invest) is always going to have a poor performing sub-investment and our brains are quite good at finding and stressing over them. You can be successful with an allocation strategy if you can look at the entire strategy rather than each component and tell yourself that the whole is performing better than you is likely when focusing on the parts. You have to train your brain to ignore the “not working” periods. You can allocate aggressively or conservatively - the more stocks (aggressive) the more likely you will achieve a higher return - and the more volatile and twitch-inducing. In order to stay with the same strategy over long periods, you will need to rebalance to the original strategy on occasion. As you get closer to potentially withdrawing funds for income ( what we call decumulation, versus accumulation during your earning years) you may want to consider a more conservative allocation (you might not if you have accumulated excess wealth/capital). If this is a taxable investment account, you will want to harvest tax losses, also.

As the data and the discussion demonstrate, this is all operationally relatively simple and behaviorally difficult.

Thanks for reading. All feedback is a gift.

Sundry

My father celebrated his 100th birthday this week. His health is rapidly declining, sadly - but he made it.

I just finished reading Crook Manifesto, a great fiction read and interesting look at Harlem in the 1960’s and 1970’s.

I also watched Summer of Soul this past week, which was held in Mount Morris Park. Crook Manifesto is set in the same area, so the intersection was a fascinating coincidence. Something here about correlation and causation?

We finished Hijack last week. Definitely worth watching if you like suspense.